Getting Crowded

November 6, 2025

Jake Keys | jake.keys@appalachescapital.com

Lately, AI capital expenditure estimates have been scaling rapidly. Very rapidly. As of this past quarter, the combined quarterly capital expenditures of Meta, Alphabet, Amazon, and Microsoft exceeded $100 billion. Like a black hole, as more and more resources are committed, the need for more resources grows further. These resources are also scarce. Only so many silicon wafers, only so many tons of cement, and only so much power can be produced to satisfy the needs of the broader economy. At this point, it is fair to ask, “Is the AI boom crowding out the rest of the economy?”

“Crowding out” has traditionally referred to the phenomenon of rising interest rates due to excessive government spending, which subsequently leads to less private investment and economic stagnation. However, the term has evolved over time to include other spending with similarly influential gravity, such as coordinated spending within a private sector industry. Typically, this is discussed in the context of interest rates – a large amount of borrowing by anyone can lead to higher market rates for all. However, this can analogously be applied to other resources as well. If economics is the study of how scarce resources are produced and distributed, “crowding out” is when those scarce resources are overwhelmingly consumed by a limited number of firms, driving up costs for everyone else and limiting growth elsewhere.

Economists with Bloomberg suggest that AI investment could contribute upwards of 1.5 percentage points to GDP growth next year, based on the current capital expenditure guidance from Meta, Alphabet, Amazon, and Microsoft. That’s about all of the forecasted growth in GDP the OECD has put out for the U.S. in 2026. If AI is contributing most of the growth, then the non-AI part of the economy is stagnating or declining. However, if AI is in fact crowding out the rest of the economy, then in its absence, rates could be lower and other parts of the economy would be stronger; a sanguine point to consider for those who are pessimistic about the situation. But what would happen if that situation were to change?

I’ve been tossing around roughly two main questions in my head:

1) Is the AI boom crowding out the rest of the economy?

and,

2) What are the implications over the intermediate to long-term if so?

Crowding out?

You could reasonably point to two different kinds of capital that massive AI related spend could be crowding out: physical capital and financial capital. I think it is very likely, if not certain, that data center projects are crowding out physical resources. However, this seems unlikely as it relates to financial capital, since most of the spending so far has been self funded. Yet, as we have seen recently, this may be changing with hyperscalers turning to the bond market for financing.

AI Crowding Out Physical Capital

The crowd out of physical resources from datacenter construction is clear. The most obvious is the situation regarding computing hardware. Foundry capacity has been dedicated to producing leading edge chips for datacenters, which has reduced the supply of trailing edge chips, or at the very least contributed to a continued shortage in these chips relative to their demand.

Take, for example, the automotive industry. Chip shortages for OEMs began over five years ago, and supply has not been consistent since. With more demand coming from leading edge nodes, chip suppliers are choosing to prioritize these customers which has led to a lack of attention to ongoing chip shortages. Modern automobiles also use DRAM and NAND, which have also increased in price on the heels of the data center buildout, and has led to OEMs having to accept higher prices, longer lead times, and lower supply.1

Secondary to chip demand, look at how the data center buildout has contributed to higher energy prices. Reporting from Bloomberg suggests that monthly energy bills are upwards of 267% higher than they were just five years ago in areas near significant data center activity. While their story focuses on what this means for consumers, this effect carries over to other industries in the area as well. This is potentially a source of margin pressure that makes investment unattractive for those that are not participating in the buildout.2

Could AI Crowd Out Financial Capital?

Unlike physical resources, the consequences of crowding out in financial capital are less clear, or have simply not occurred yet. A large part of this has to do with the method in which the data center buildout has been financed so far. Rather than raising external capital, these investments have mainly been funded through the internal cash flows of Alphabet, Meta, Amazon, and Microsoft. However, this seems to be changing, as Meta, Oracle, and Alphabet have each announced their own bond offerings totaling over $140 billion this year.3 That number is only expected to grow, but even so, corporate credit spreads are near all-time lows. While it could happen in the future, it does not seem that we are seeing any crowding out in the credit market just yet.

However, could a case be made that the equity market is being crowded out? Probably not in the traditional sense. As many current market apologists would point out, IPO activity is still low relative to history, and while the secondary market is clearly favoring AI-related firms, this has little impact on the capital raised outside of companies active in secondary offerings. Instead, this is more indicative of the crowding out of mind share for investors. The focus over the last few years has increasingly been on these AI-related firms, and today, it seems as though the rest of the market is being tossed aside. Over the last few months, it has almost seemed as if AI stocks are not just being fervently bid up, but shares in companies with no exposure are being sold to fund the trade. This capital flight from the old economy to the new economy may not have much impact on capital raising per se, but it will impact an executive’s decision to build a new factory or to repurchase their cheap equity if it persists.

Private Investment Data Paints a Clearer Picture

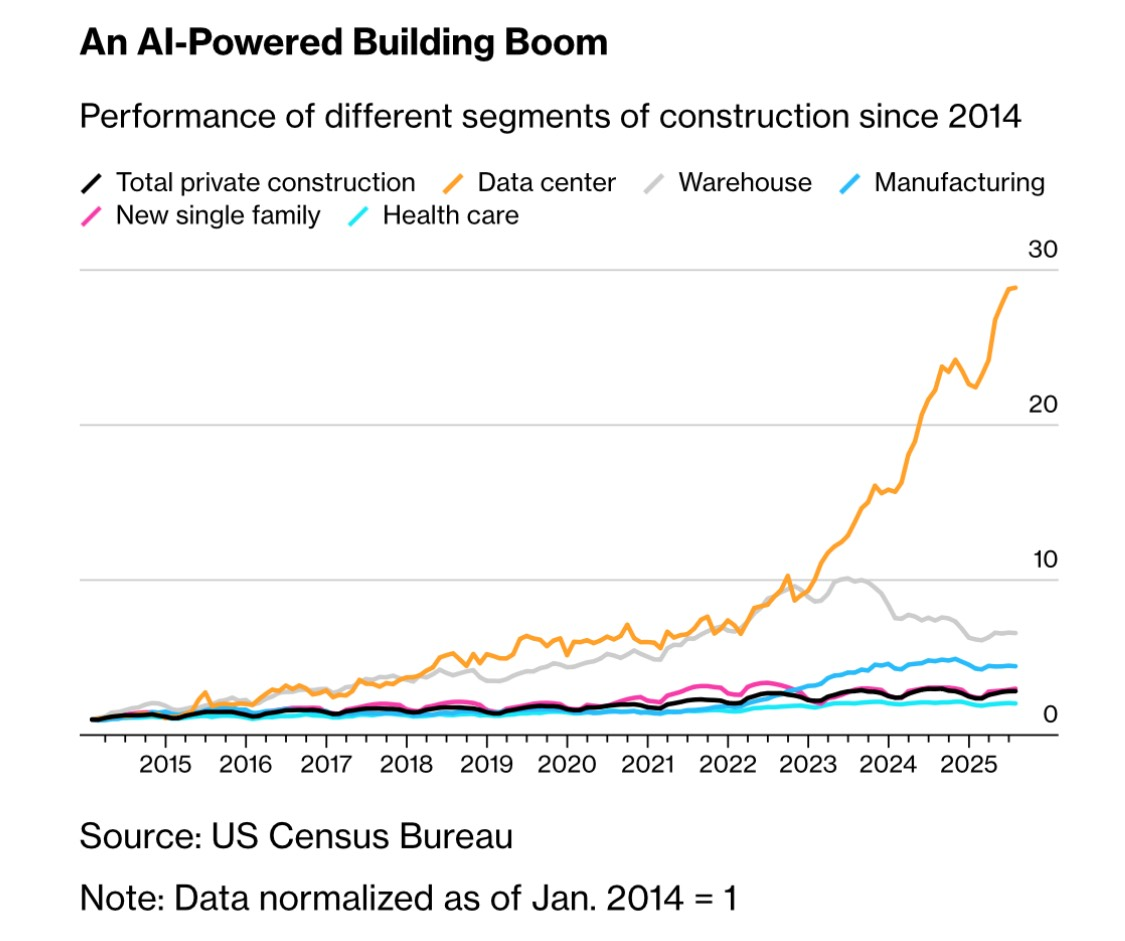

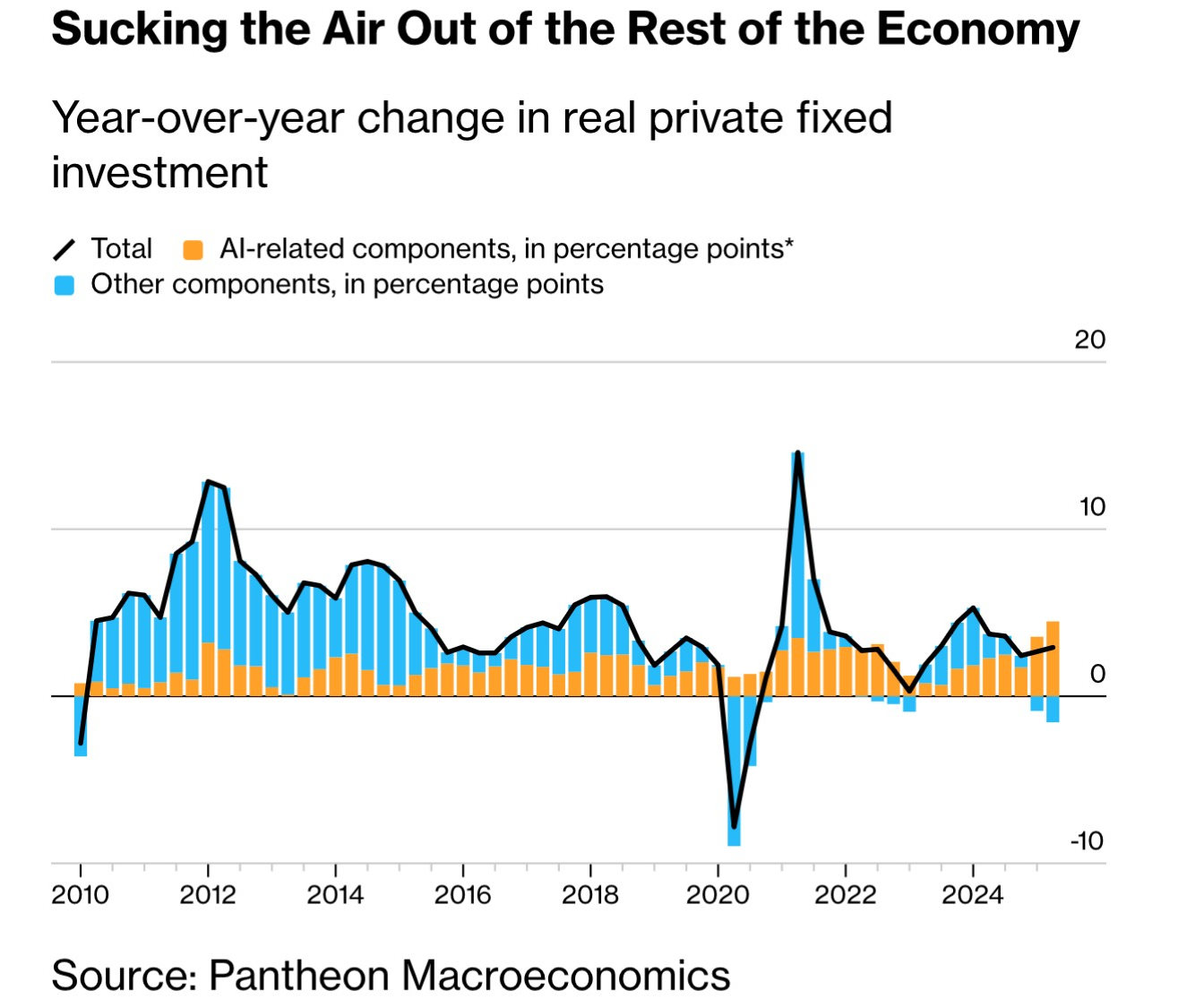

On one hand, you have clear signs of the data center buildout impacting the costs of certain commodities and products. On the other hand, you have to make some leaps of faith to claim that financial capital is being crowded out. Yet, private construction and investment data paints a clearer picture of the divergence between the data center economy and everything else. Here are two charts sourced from Bloomberg, using data from the U.S. Census Bureau and Pantheon Economics:

Private construction data shows that data center construction has continued to grow after the 2020 and 2021 stimulus cycle, while most other segments are in stagnation. Data center construction expenditures are nearly 30 times larger than they were in 2014.4 The fixed investment data shows that over the last few quarters, investment in non-AI related assets is shrinking year-over-year.5 This supports the idea that there is very likely some level of crowding out occurring.

What are the impacts?

The most obvious consequence of crowding out is a reduction in investment from outside firms. This can lead to a reduction in earnings growth, but episodes of crowding out have historically been short-term in nature, making these reductions short-lived. Long-term, it seems that the consequences of private sector crowding out are most significant for the inside firms that are leading investment. Too much capital flowing into an industry experiencing high returns will inevitably reduce those returns.

Another consequence of private sector crowding is an increased level of concentration in the economy. This is risky, because problems that would normally be limited in scope have a magnified impact on the aggregate. In the telecommunications boom of the late 1990s, a similar situation unfolded. When the infrastructure was inevitably overbuilt, investment in the industry came to a halt and the top-heavy economy entered a recession in 2001.

Still, there were some positive corners of this investment-led recession. While private investment fell, mainly due to the largest contributors in prior years scaling back, consumption did not. The consumer was nearly unaffected by the whole ordeal. Yes, unemployment rose to 6% from 4%, but personal consumption expenditures remained robust.6 In fact, many of the companies that had been starved of capital over prior years were able to pick up the slack as investors rotated capital back in their favor.

The market crash of 2000-2002 was arguably more severe than the actual recession. This was mainly driven by high levels of index concentration, and a large majority of individual stocks outperformed the index in the following years. In the year 2000 specifically, six out of ten of the S&P 500 sectors were positive, even though the index itself was down. While the entire market could not avoid the ensuing recession, sectors not a part of the highly concentrated new economy and market greatly outperformed their counterparts in 2001 and 2002.7

Investors who are uneasy about crowding out may rest a little easier knowing that capital can be released back into sectors that are currently unassuming, acting as a long-term source of resiliency for the economy as a whole. It certainly seems as though some industries are being crowded out, but there is still some room left to be optimistic. Short term episodes of capital flight do not have to result in long-term changes in fundamental value for firms that should be otherwise unimpacted. If anything, the historical scoreboard has been in favor of focusing on firm specific fundamentals, and not trying to game near term investor preferences.

Endnotes:

- https://www.spglobal.com/automotive-insights/en/blogs/2025/10/semiconductor-tug-of-war-ai-data-centers-automakers ↩︎

- https://www.bloomberg.com/graphics/2025-ai-data-centers-electricity-prices/ ↩︎

- According to the company filings of Meta, Oracle, Alphabet, and Amazon and as calculated by Appalaches Capital. ↩︎

- https://www.bloomberg.com/news/features/2025-10-24/ai-data-center-boom-threatens-trump-s-manufacturing-revival ↩︎

- https://www.bloomberg.com/news/newsletters/2025-10-24/the-dark-side-of-the-ai-boom-is-it-s-masking-weak-investment ↩︎

- U.S. Bureau of Economic Analysis ↩︎

- According to market data and as calculated by Appalaches Capital. ↩︎

Important Disclosures

This page is provided for informational purposes only. The information contained in this page is not, and should not be construed as, legal, accounting, investment, or tax advice. References to stocks, securities, or investments in this page should not be considered investment recommendations or financial advice of any sort. Appalaches Capital, LLC (the “Firm”) is a Registered Investment Adviser; however, this does not imply any level of skill or training and no inference of such should be made. All investments are subject to risk, including the risk of permanent loss. The strategies offered by Appalaches Capital, LLC are not intended to be a complete investment program and are not intended for short-term investment. Any opinions of the author expressed are as of the date provided and are additionally subject to change without notice.