Monthly Mentions

July 2025

A lot happens over the course of a quarter. Not all of it makes it into the letter. Monthly Mentions are short and informal posts that highlight a few of the most interesting headlines for the month.

“Union Pacific and Norfolk Southern to Create America’s First Transcontinental Railroad”

Union Pacific Press Release (7/29/2025)

After weeks, if not months, of railroad mega-merger rumors, the announcement finally came: Norfolk Southern has accepted an offer to be acquired by Union Pacific. If you had asked me whether another major railroad merger would ever be approved after the Canadian Pacific and Kansas City Southern deal in 2023, I would have said the odds were slim to none. With only six Class 1 railroads across the U.S. and Canada, all operating in an effective duopoly within their shipping corridors, competition is far from fierce. Yet, the current Surface Transportation Board seems open to seriously considering the merits of even further consolidation.

If this merger is approved, the new Union Pacific should enable coast-to-coast rail service in the U.S. to flourish. Instead of having to make an interchange in Chicago (a process which can take a full 24-48 hours), transcontinental bound trains should be able to roll right through or avoid the hub entirely. Every hand-off from one network to another adds significant time and costs, so having larger networks is attractive from this point of view. Yet, if Union Pacific and Norfolk Southern are permitted to merge, BNSF will inevitably have to merge with CSX to create a competitive service. This merger does not seem like it would be beneficial for competition between the rails, but does that necessarily mean that it won’t go through? The announcement uses language like “America’s First Transcontinental Railroad”, “Enhances U.S. Competition”, and “Advances America’s domestic manufacturing”, all of which seems to fit right in with the ethos of the current administration and its goals. It is a shareholder presentation, but the rhetoric is very much geared towards pleasing a regulatory audience.

Boring industries can quickly become very interesting.

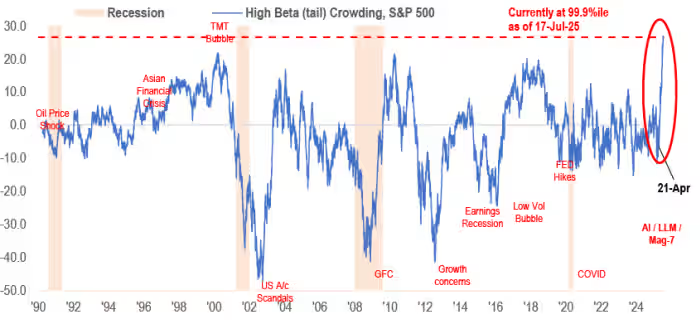

“High Beta Crowding at ~100%ile”

J.P. Morgan Equity Strategy & Quant Research (7/17/2025)

Source: J.P. Morgan Equity Strategy & Quant Research

Over the past several weeks, as the market has marched higher, investors have piled into quantifiably riskier stocks. As J.P. Morgan notes, crowding in “High Beta” stocks is at the 99.9th percentile. The debate is still out as to whether beta itself is a good measure of risk, but it is a measurement of a stock’s relative volatility and correlation with the broader index. It is, at least, a clear indication of that much. Stocks with higher measured betas tend to be less profitable, have worse balance sheets, and are more levered to the economy. Now, there are of course many exceptions (we own some), but this is true for the group on average. It is certainly possible to find great companies with high betas, but the base rate is lower.

There is a price for every asset, including businesses that are unprofitable. However, when unprofitable, debt-encumbered, or otherwise lower quality businesses are bid up in a frenzy, it can be puzzling. Sometimes, the reaction makes sense. After the Great Financial Crisis in 2008, unprofitable businesses had been crushed and left for dead. With fiscal stimulus they quickly became viable again. Other times, however, this crowding can only be explained by unbridled optimism. Leading up to the bursting of the Dot Com Bubble in 2001, investors had also crowded into high beta stocks. At that time, it was simply driven by a fear of missing out on the new economy while watching the prices of speculative growth stocks go up day after day.

It is my opinion that the recent move is disconnected from any fundamental support. I am instead interested in other areas of the market where opportunities are more likely to be found. I find it important in times like these to resist the FOMO and lean into standing apart from the crowd.

Endnotes:

Important Disclosures

This page is provided for informational purposes only. The information contained in this page is not, and should not be construed as, legal, accounting, investment, or tax advice. References to stocks, securities, or investments in this page should not be considered investment recommendations or financial advice of any sort. Appalaches Capital, LLC (the “Firm”) is a Registered Investment Adviser; however, this does not imply any level of skill or training and no inference of such should be made. All investments are subject to risk, including the risk of permanent loss. The strategies offered by Appalaches Capital, LLC are not intended to be a complete investment program and are not intended for short-term investment. Any opinions of the author expressed are as of the date provided and are additionally subject to change without notice.